Loan approval feels unpredictable for many borrowers. One lender moves quickly, another stalls for weeks, and the reasons aren’t always clear.

A major factor behind that inconsistency is underwriting itself and how differently institutions handle it. Only about 13% of banks have adopted AI in their credit and lending processes, meaning most loan decisions still rely heavily on manual reviews and legacy systems.

That gap explains why underwriting can feel slow, document-heavy, and opaque. It’s also why loan terms, conditions, and timelines can vary so widely, even for similar borrowers.

In this blog, we will discuss loan underwriting in clear, practical terms. You’ll learn the different types of underwriting, how the process works step by step, and why understanding it can help you prepare better, avoid delays, and make smarter financing decisions.

What Is Loan Underwriting?

Loan underwriting is the structured evaluation lenders use to decide whether a loan fits their risk standards and under what terms. At this stage, the focus shifts from collecting information to validating it, checking accuracy, consistency, and alignment with the lender’s credit guidelines.

Underwriting examines how different elements of an application work together. Income, existing obligations, asset strength, and, when applicable, collateral quality are reviewed in context. The goal is to determine repayment reliability across expected conditions, not best-case scenarios.

This is also where pricing and structure take shape. Interest rates, loan size, covenants, loan-to-value ratio reserves, and conditions are adjusted based on the risk profile that emerges during review. When underwriting is thorough, outcomes are clearer: approvals come with fewer surprises, and declines are grounded in specific, explainable factors rather than ambiguity.

Types of Loan Underwriting

Lenders use different approaches depending on loan size, complexity, risk tolerance, and speed requirements. Some rely heavily on human judgment, others on technology, and many combine both. Understanding the main underwriting types helps borrowers set realistic expectations around timelines, documentation, and decision-making.

Manual Underwriting

Manual underwriting relies on experienced underwriters reviewing financial documents, credit history, and supporting materials line by line. This approach allows for deeper context, especially when a borrower’s profile doesn’t fit standard formulas. Income variability, unique assets, or nontraditional business models can be evaluated with flexibility rather than being flagged automatically.

Because people, rather than systems, make decisions, manual underwriting can account for compensating factors such as strong liquidity, consistent cash flow trends, or relevant experience. The tradeoff is time. Manual reviews often take longer and may involve multiple clarification requests.

Manual underwriting is commonly used for:

- Commercial real estate loans

- Business and investment loans

- Borrowers with complex or nontraditional financial profiles

Automated Underwriting

Automated underwriting uses software and algorithms to assess risk based on predefined rules and data inputs. Applications are processed quickly by comparing borrower information against established credit models. This approach is efficient and consistent, making it ideal for high-volume, standardized loans.

Because automated systems depend on data thresholds, they work best when borrower profiles are straightforward, and documentation is clean. However, they leave little room for nuance. Irregular income, one-time events, or atypical assets may trigger declines even when overall risk is manageable.

Automated underwriting is most common in:

- Conventional residential mortgages

- Personal loans and consumer credit

- Auto loans

Where Each Type Is Typically Used

Most lenders don’t rely on a single method across all products. Instead, underwriting style aligns with the loan purpose and risk profile.

- Mortgages: Often begin with an automated review and document request process, followed by human oversight

- Business loans: Frequently use manual or hybrid approaches

- Personal loans: Primarily automated due to volume and standardization

Knowing which underwriting type applies to your loan can help you prepare better and avoid surprises as your application moves forward.

What Does the Loan Underwriting Process Entail?

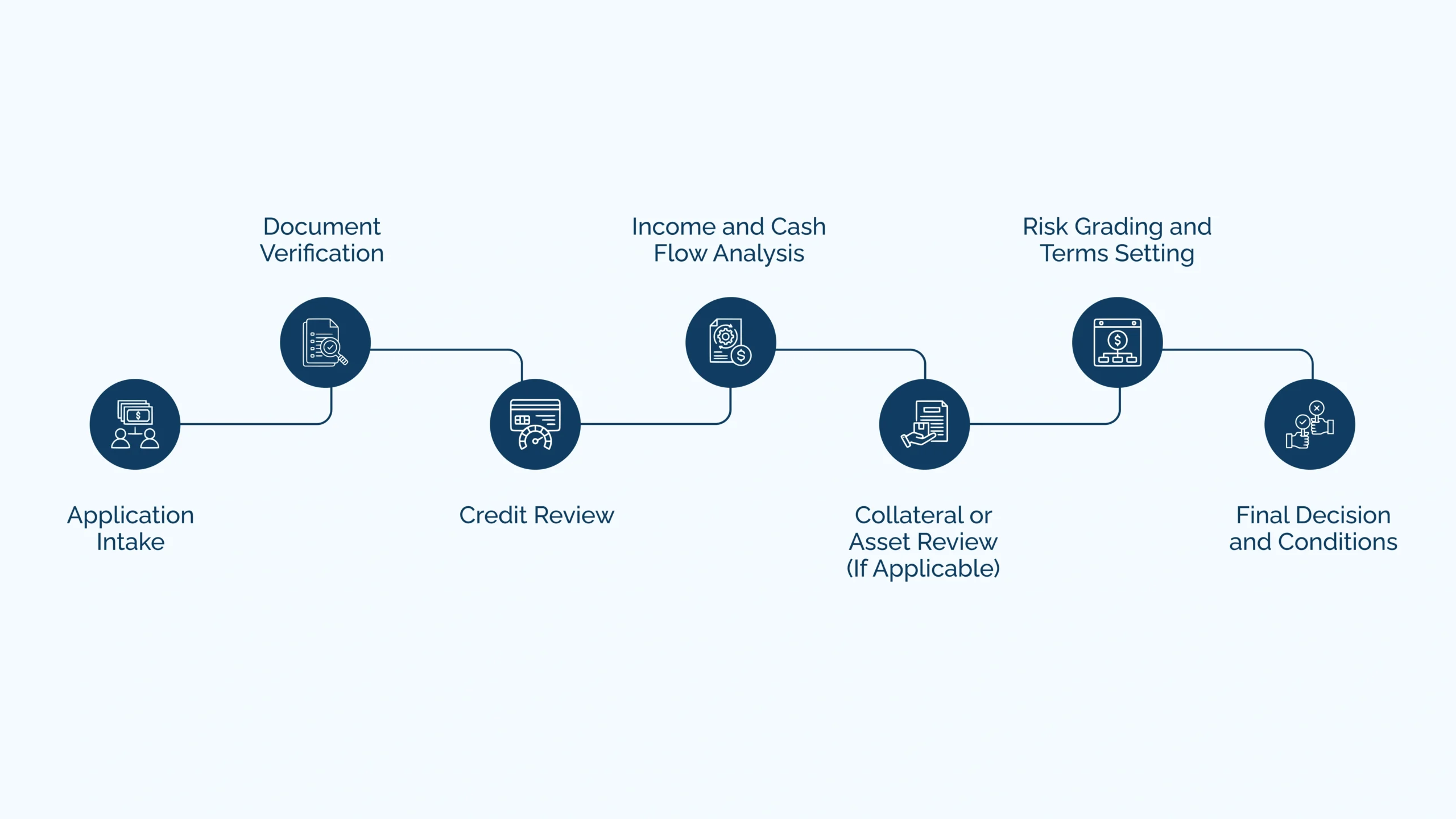

Once an application moves into underwriting, the focus shifts to verification and risk alignment. While specifics vary by lender and loan type, the process generally follows a consistent sequence to confirm accuracy, assess exposure, and finalize terms.

- Application Intake: The lender reviews the submitted application to ensure it’s complete and aligns with basic eligibility criteria. Missing items are flagged early to prevent downstream delays.

- Document Verification: Financial documents are validated for accuracy and consistency. Underwriters look for gaps, discrepancies, or unsupported figures that need clarification.

- Credit Review: Credit reports are evaluated to understand payment history, outstanding obligations, and overall credit behavior. Patterns matter more than isolated events.

- Income and Cash Flow Analysis: Underwriters assess the stability and sufficiency of income (or business cash flow) relative to the requested loan. Sustainability is prioritized over one-time spikes.

- Collateral or Asset Review (If Applicable): For secured loans, property or asset details are reviewed to confirm condition, ownership, and market support for the loan amount.

- Risk Grading and Terms Setting: Based on the full picture, the lender assigns a risk profile and adjusts loan size, pricing, reserves, or conditions accordingly.

- Final Decision and Conditions: Approval, conditional approval, or decline is issued. If approved, any remaining conditions must be satisfied before closing.

Understanding this flow helps borrowers anticipate requests, respond faster, and keep the process moving smoothly.

Major Factors Loan Underwriters Evaluate

Underwriters don’t assess applications in isolation. Each factor is reviewed in relation to the others to understand overall risk, consistency, and repayment capacity. Knowing what receives the most scrutiny can help borrowers prepare more effectively and reduce back-and-forth during review.

- Credit Profile: Payment history, credit utilization, and the mix of existing obligations are examined to identify patterns. Occasional issues may be outweighed by long-term consistency, while recurring problems raise concerns.

- Income Stability or Cash Flow: Underwriters look at how reliable income sources are over time, not just current levels. For businesses, trends and sustainability often carry more weight than short-term performance.

- Debt Obligations: Existing liabilities are reviewed to determine how much additional debt the borrower can reasonably support. The focus stays on balance, not maximum leverage.

- Liquidity and Reserves: Available cash or liquid assets provide a buffer against unexpected disruptions. Strong reserves often strengthen an application, especially in tighter credit environments.

- Collateral Strength (When Applicable): For secured loans, asset quality, condition, and marketability influence comfort levels and loan structure.

Each of these elements contributes to the final risk profile, shaping both approval outcomes and loan terms.

Benefits of Understanding the Underwriting Process

Here are the benefits of understanding the underwriting process:

Faster, Smoother Approvals

Borrowers who understand underwriting know what documentation matters and how it will be reviewed. That awareness reduces incomplete submissions, limits follow-up requests, and keeps the application moving. Clear, well-prepared files help underwriters work efficiently, which often translates into shorter review cycles and fewer last-minute surprises before approval or closing.

Stronger Loan Terms

Underwriting determines pricing, structure, and conditions. When borrowers anticipate how risk is evaluated, they can position their application more effectively. Stronger preparation around cash flow, reserves, or collateral can support better interest rates, higher loan amounts, or more flexible terms aligned with their financing goals.

Better Decision-Making Before Applying

Understanding underwriting criteria helps borrowers assess their readiness before submitting an application. That insight helps avoid applying too early, requesting the wrong loan structure, or choosing an unsuitable lender. As a result, borrowers pursue financing that fits their profile, improving outcomes and reducing unnecessary credit pulls or declined applications.

Reduced Stress and Uncertainty

Much of the frustration around lending comes from not knowing what’s happening behind the scenes. Familiarity with underwriting removes that uncertainty. Borrowers know what to expect, why questions are being asked, and how decisions are reached, making the process more predictable and far less stressful overall.

Secure Financing with a Partner Like Bluestone Capital Who Understands the Process

Loan underwriting doesn’t have to slow your deal down when you work with a lender that values clarity, speed, and alignment. At Bluestone Commercial Capital, we believe lending decisions should be guided by experienced professionals, not automated systems. Every opportunity is reviewed through a manual underwriting process, allowing our team to carefully evaluate the details of each project, borrower, and timeline.

This hands-on approach ensures deals are assessed on their true merits rather than relying solely on rigid algorithms. It also allows us to maintain efficiency while providing the careful review that serious real estate and commercial investments require.

Here’s how Bluestone supports your next move:

- Fast, streamlined approvals supported by experienced underwriting professionals for time-sensitive opportunities

- Flexible bridge loans for acquisitions, transitions, or short-term gaps

- Fix-and-flip financing tailored to value-add strategies

- Clear guidance throughout the lending process so expectations stay aligned

When you’re ready to move forward with confidence, Bluestone is here to help you secure capital on terms that fit your strategy. Let’s talk about your next opportunity.