Commercial loan brokers operate in a market full of demand, but access to capital is uneven. Borrowers come in with viable projects, strong intent, and clear timelines, yet many requests never translate into funded deals. In fact, only 31% of small businesses receive the full loan amount they request from banks. The reason is simple: the right lender match isn’t always within reach.

Conventional lenders remain selective, programs change quickly, and underwriting appetites vary by asset type, geography, and timing. Without multiple funding paths, even solid transactions can stall.

A strong lender network gives brokers control over outcomes. It allows you to reroute deals, adjust structures, and keep momentum when one option falls short. Instead of relying on a single approval path, you operate with flexibility and confidence.

In this blog, we will focus on how to find lenders, build productive relationships, and develop a lender network that supports consistent closings across a wide range of commercial financing scenarios.

Why Your Lender Network Is Important for Your Brokerage

Every commercial loan brokerage runs on one central engine: its lender relationships. These connections determine which deals move forward, how quickly they close, and how often clients return with repeat business. Without reliable access to capital sources, even the most capable brokers find their pipelines narrowing.

A strong lender network allows you to respond decisively when borrowers’ needs fall outside standard boxes. Instead of forcing deals into mismatched programs, you can identify lenders whose criteria align with the transaction. That flexibility improves approval rates, shortens turnaround times, and strengthens your credibility with clients.

As your network expands, so does your ability to negotiate terms, manage risk, and handle more complex requests. Over time, lender access becomes the difference between reacting to constraints and shaping outcomes, making it one of the most valuable assets your brokerage can develop.

What a High-Quality Lender Network Actually Looks Like

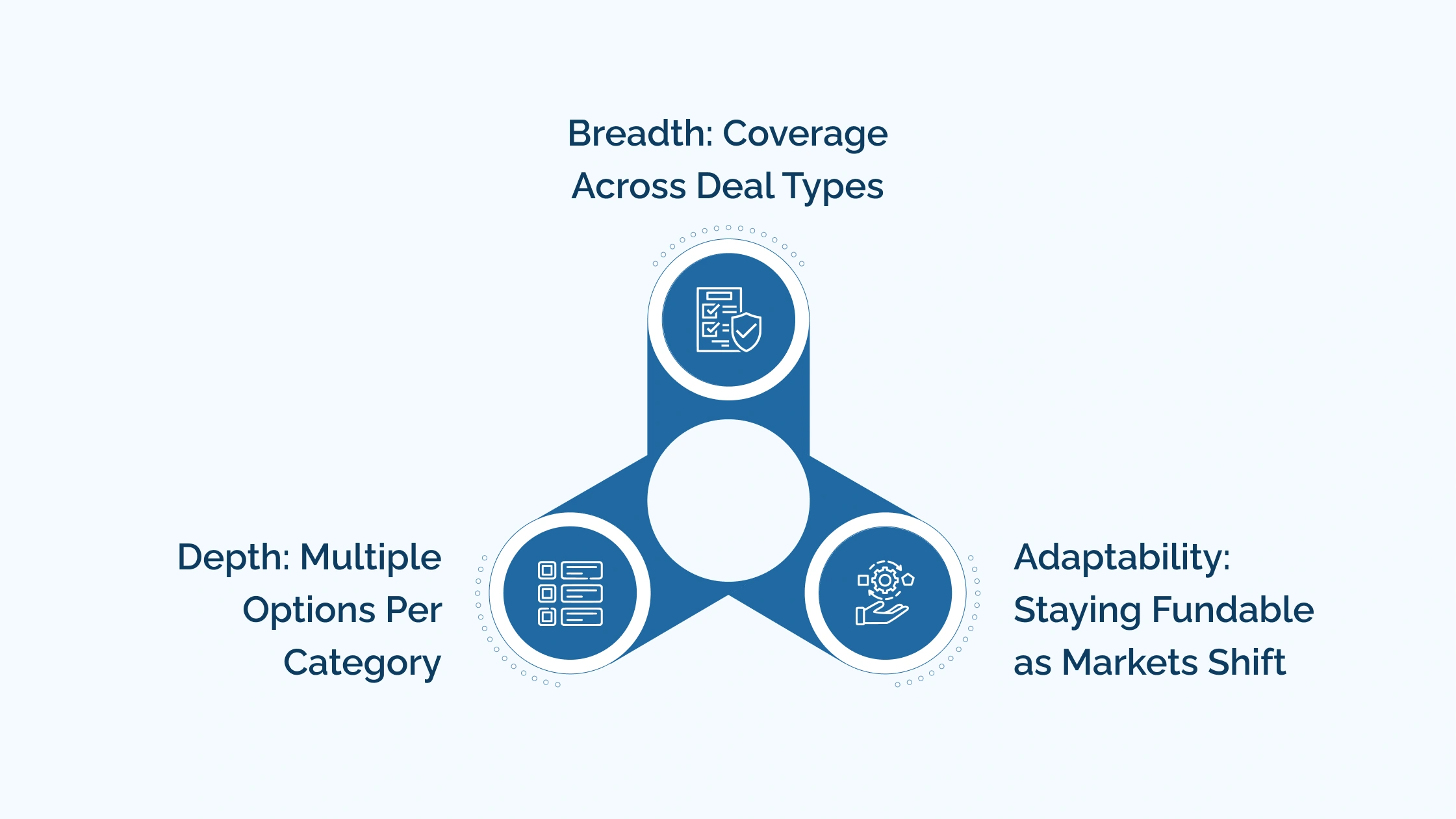

A lender network isn’t measured by how many contacts sit in a CRM. Quality comes from structure. The strongest broker networks are intentionally built to handle variety, volume, and change without friction. That means coverage across deal types, multiple funding paths per category, and the ability to stay relevant as lender appetites evolve.

Breadth: Coverage Across Deal Types

High-performing brokerages aren’t built around a single product vertical. Borrower needs shift quickly, and deals often evolve mid-process. A network with real breadth allows you to place financing across asset classes without forcing transactions into ill-fitting programs.

Single-lane networks fail brokers over time because they cap what you can serve. When all roads lead to one type of lender, every deviation becomes a dead end. Breadth ensures you can say “yes” more often and mean it without compromising deal quality or timelines.

Depth: Multiple Options Per Category

Depth means having more than one lender willing to look at the same type of deal. That redundancy protects your pipeline when a lender pauses funding, tightens criteria, or slows response times. It also reduces the risk associated with internal changes you don’t control, such as staffing shifts or capital reallocations.

Negotiation leverage comes directly from depth. When lenders know you have alternatives, conversations change. Terms improve, turnaround speeds up, and exceptions become more realistic. Backup options keep deals alive when the first answer isn’t the right one.

Adaptability: Staying Fundable as Markets Shift

Lender criteria are never static. Asset classes fall in and out of favor, geographic focus shifts, and risk tolerance adjusts with economic cycles. A high-quality network reflects that movement rather than resisting it.

Static networks quietly decay. Programs expire, contacts go stale, and once-reliable lenders become mismatched without obvious warning signs. Adaptability requires active relationship management, ongoing outreach, and regular reassessment of who is funding what, so your brokerage remains fundable regardless of market conditions.

Types Of Commercial Lenders And How They Operate

Every lender follows a distinct operating model that influences how quickly they move, what they approve, and how flexible they can be.

Conventional Banks and Credit Unions

These institutions lend depositor capital and operate under strict regulatory oversight. Their underwriting favors predictability and long-term performance.

- Capital Source: Funded primarily by customer deposits and balance-sheet lending

- Risk Profile: Conservative, with limited tolerance for transitional assets

- Underwriting Focus: Cash flow history, borrower financial strength, and property stability

- Timeline: Longer approval and closing processes

- Best Use Case: Stabilized properties and borrowers with strong financials

Private and Non-Bank Lenders

Private lenders deploy investor or fund capital and operate with broader discretion around structure and risk.

- Capital Source: Private funds, family offices, or institutional investors

- Risk Profile: Higher tolerance for complexity and transitional situations

- Underwriting Focus: Asset value, exit strategy, and deal viability

- Timeline: Faster approvals and closings

- Best Use Case: Time-sensitive transactions, stabilizing a property, pulling cash-out, or non-conforming deals

Platform and Marketplace Lenders

These entities function as distribution channels, routing deals to multiple capital sources through a single intake.

- Role: Technology-driven intermediary rather than direct lender

- Process: One submission matched across several lender programs

- Efficiency: Streamlined intake and initial screening

- Limitations: Less transparency and control over final credit decisions

- Best Use Case: High-volume or standardized financing requests

Specialty and Niche Lenders

Specialty lenders focus on narrow asset classes or financing purposes and bring deep expertise to specific deal types.

- Focus Area: Equipment, SBA, healthcare, franchise, or industry-specific lending

- Expertise: Detailed understanding of niche underwriting risks

- Program Structure: Highly defined criteria and documentation requirements

- Flexibility: Strong within the niche, limited outside it

- Best Use Case: Borrowers with specialized financing needs

Knowing how each lender type operates allows brokers to place deals with precision, avoid misalignment, and maintain credibility throughout the financing process.

Top 6 Ways to Find Reliable Commercial Lenders

The right approach to finding lenders prioritizes fit, reliability, and long-term viability, ensuring every new lender strengthens your ability to place loans efficiently and close with confidence.

1. Join an Established Lender Network

An established lender network provides immediate access to vetted, broker-friendly lenders across multiple financing categories. Instead of spending months building relationships one at a time, you step into an ecosystem where lenders already understand how to work with brokers and actively fund deals.

These networks reduce trial-and-error, improve response times, and expose you to lenders with proven closing track records. They also provide insight into current lending appetites, program changes, and real-world performance, helping you place deals more efficiently from day one.

2. Strategic Online Research

Online research works when it’s intentional and targeted. Rather than broad searches, focus on identifying lenders that actively work with brokers and fund the types of deals you handle.

Major areas to evaluate during online research include:

- Broker Programs: Confirmation that the lender explicitly works with third-party brokers

- Active Deal Types: Loan sizes, asset classes, and borrower profiles they currently fund

- Geographic Coverage: States or regions where capital is actively deployed

- Decision Process: Clarity on underwriting timelines and approval authority

- Recent Activity: Evidence of recently closed transactions or program updates

This approach helps filter out lenders that look good on paper but don’t align with real-world deal placement.

3. Social Platforms and Direct Outreach

Social platforms allow brokers to bypass generic submission portals and connect directly with decision-makers. Used correctly, they provide visibility into lender activity, program changes, and real-time appetite shifts.

Effective outreach focuses on intent and relevance:

- Targeted Contacts: Business development officers and broker relationship managers

- Contextual Messaging: Referencing specific programs or recent lender activity

- Engagement First: Interacting with lender content before initiating outreach

- Clear Purpose: Opening conversations around real deal scenarios, not general introductions

Direct, informed outreach builds credibility quickly and increases response rates compared to cold submissions.

4. Industry Events and Conferences

Industry events and conferences create opportunities to build lender relationships that move faster than digital outreach. Face-to-face conversations allow brokers to understand lender priorities, risk tolerance, and deal preferences in a short amount of time. These settings also make it easier to establish rapport and credibility early in the relationship.

The real value comes after the event. Brokers who schedule follow-up conversations, reference specific discussions, and align future submissions with stated lender appetites turn brief introductions into productive, long-term partnerships.

5. Professional Associations and Directories

Professional associations and lender directories provide structured access to funding sources that actively participate in the commercial finance ecosystem. These organizations often curate member lists, publish program details, and host networking opportunities that help brokers identify credible lenders more efficiently.

Membership also adds legitimacy when initiating contact. Lenders are more receptive when outreach comes through recognized industry channels, and directories help brokers focus on institutions that are actively deploying capital rather than passively advertising programs.

6. Referrals From Industry Peers

Referrals from trusted industry peers often lead to the highest-quality lender relationships. These introductions carry built-in credibility and shorten the trust-building phase that usually slows new partnerships.

Peers such as fellow brokers, commercial real estate agents, attorneys, CPAs, and even lenders themselves frequently know which capital sources are actively funding specific deal types. A warm referral also provides insight into how a lender performs in practice, helping you prioritize relationships that convert into funded deals rather than stalled conversations.

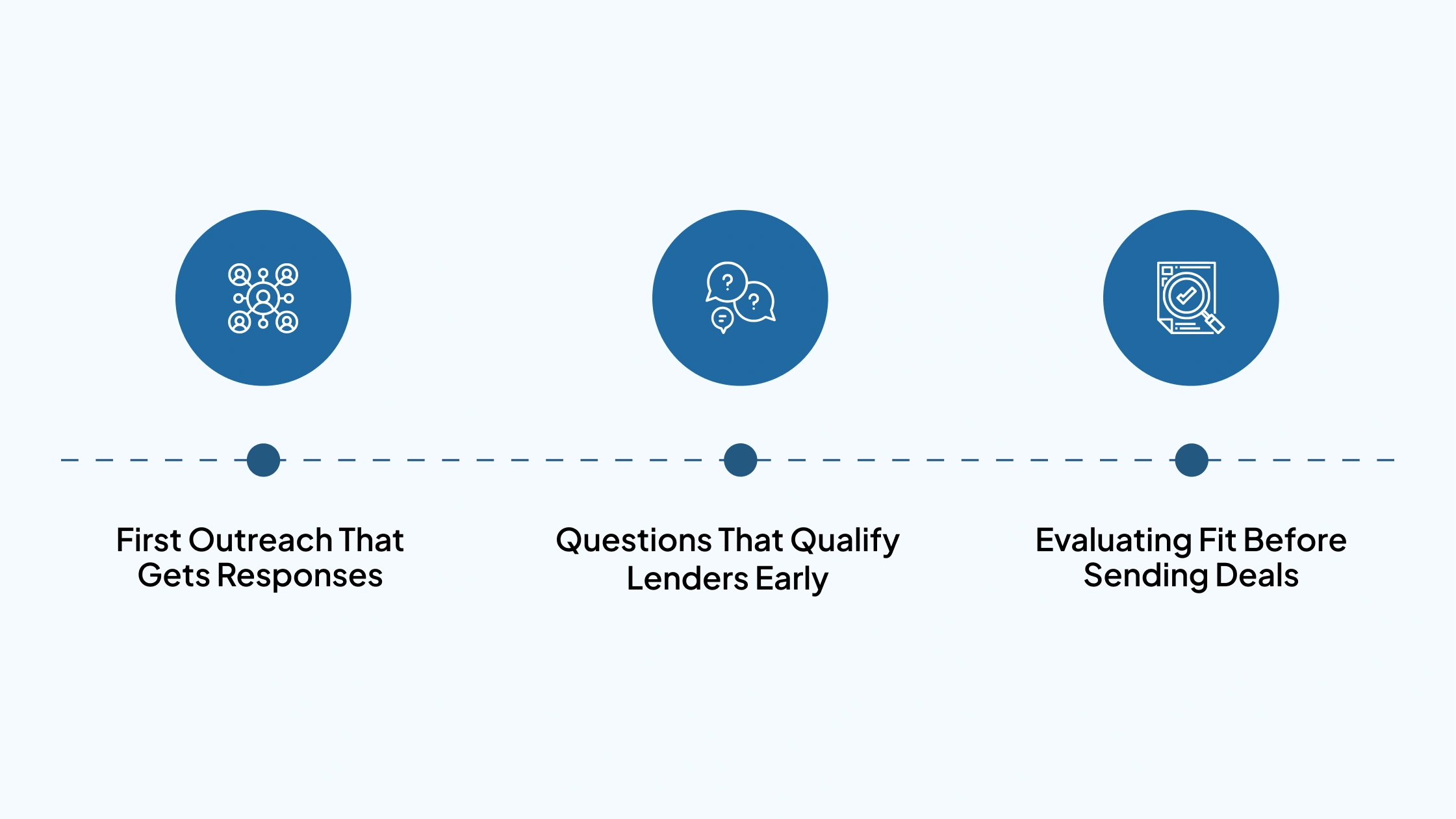

How to Approach Lenders So They Want to Work With You

Lenders decide quickly which brokers are worth their time. The difference usually comes down to how you show up in the first interaction, how clearly you understand their programs, and whether you respect their process. A thoughtful approach positions you as a partner.

First Outreach That Gets Responses

The goal of initial contact is to start a conversation around fit, not to ask for favors.

- Who to Contact: Business development officers or broker relationship managers, not generic inboxes

- How to Lead: Reference a specific deal type, market, or program they actively fund

- Value Framing: Position yourself as a source of well-screened opportunities, not someone seeking access

Questions That Qualify Lenders Early

Early conversations should surface alignment before any deal is sent.

- Program Fit: Loan sizes, asset types, geography, and borrower profiles they actively pursue

- Process Clarity: Underwriting timeline, decision authority, and documentation expectations

- Broker Terms: Compensation structure, fee timing, and any broker-specific requirements

Evaluating Fit Before Sending Deals

Not every willing lender is the right partner for your business.

- Appetite Alignment: Consistency between stated criteria and actual funded deals

- Responsiveness: Speed and clarity of communication during early interactions

- Reputation and Stability: Track record with other brokers and reliability of capital sources

Approaching lenders with clarity, preparation, and respect sets the tone for long-term collaboration. When lenders trust that your submissions are relevant and well-packaged, relationships strengthen, and deals move faster.

Maintaining Strong Lender Relationships Over Time

Finding lenders is only the first step. Long-term success comes from maintaining relationships that lenders trust and prioritize. Consistency, professionalism, and clear communication turn one funded deal into an ongoing partnership.

Major practices that strengthen lender relationships include:

- Quality Submissions: Sending complete, well-organized packages that align with stated criteria

- Clear Communication: Setting expectations early and providing timely updates throughout the process

- Transparency: Flagging potential issues upfront instead of allowing surprises mid-transaction

- Reliability: Staying responsive and engaged until the deal is fully closed

- Feedback Loop: Sharing outcomes and learning from both approvals and declines

Strong lender relationships compound over time. When lenders know you respect their process and protect their time, they respond faster, offer better insight, and become more willing to support complex or time-sensitive deals.

Turn Opportunities Into Funded Transactions With Bluestone Capital

A well-built lender network gives brokers options, but pairing that network with the right capital partner keeps deals moving when timing matters most. Bluestone Commercial Capital works alongside brokers and investors who need speed, clarity, and dependable execution.

Here’s how Bluestone supports deal flow:

- Bridge financing: Fast solutions for time-sensitive acquisitions and transitional assets

- Fix-and-flip loans: Capital structured to support purchase and renovation timelines

- Commercial real estate loans: Financing options aligned with investment goals and asset strategy

- Responsive execution: Streamlined processes that help keep transactions on track

When access and execution work together, brokers close more consistently, and clients come back. Connect with Bluestone to explore financing that fits your deals and your timelines with confidence.