Bridge Loan Approval Explained: Timelines and Tips

Bridge Loan Approval Explained: Timelines and Tips

Need to close a deal quickly but don’t have time to wait for conventional financing? A bridge loan could be the perfect solution as it provides temporary, fast funding for buyers who need immediate cash to secure a property or bridge the gap until long-term financing is available.

Unlike regular loans, bridge loans are known for speed, flexibility, and efficiency, making them the preferred choice for real estate investors and developers who need quick access to capital during transitional periods. But how long does it take for a bridge loan process to be approved?

In this blog, we’ll take you through the steps and factors that shape the bridge loan approval timeline, helping you understand how to handle the process efficiently.

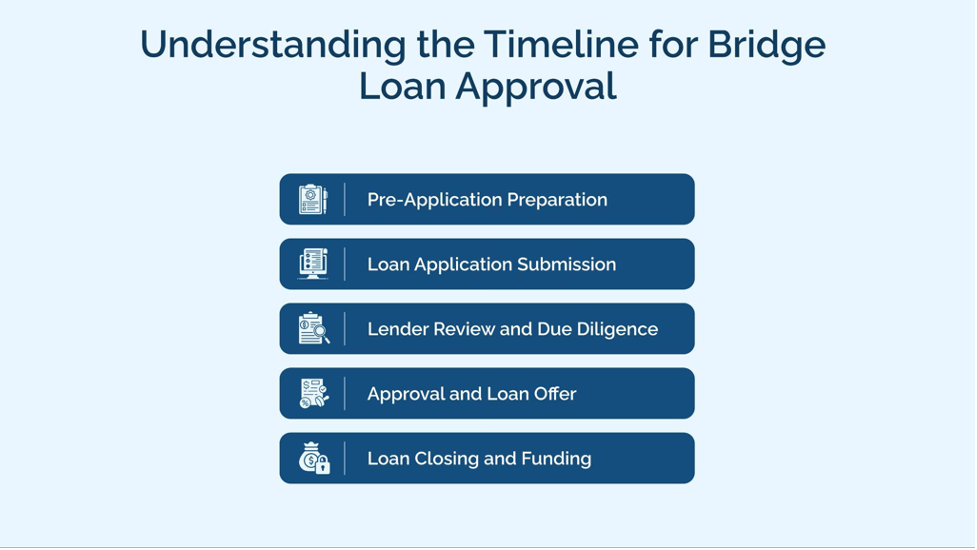

Understanding the Timeline for Bridge Loan Approval

Understanding the timeline for bridge loan approval helps investors and developers plan effectively. While the process is generally quicker than regular loans, it’s still essential to be prepared for each stage. Here are the steps to secure bridge loan approval

Stage 1: Pre-Application Preparation

Pre-application preparation is an essential first step in the bridge loan process. This stage usually takes 1 to 3 days and sets the foundation for a smooth and efficient approval process.

Property Assessment: The borrower should review the property they plan to use as collateral. This includes gathering property documentation like tax records, purchase agreements, and current appraisal reports.

Financial Overview: Lenders will evaluate the borrower’s financial situation. Investors should prepare financial statements, including cash flow projections and proof of other real estate assets.

Exit Strategy Development: A solid exit strategy must demonstrate how the loan will be repaid. The lender will expect a clear plan, whether refinancing, selling the property, or another method.

At this stage, you will need basic property details, proof of income and assets, a clear exit strategy, and preliminary documents, such as recent appraisals. This preparation ensures that the lender can evaluate the deal immediately after submitting the application.

Stage 2: Loan Application Submission

Once you’ve gathered all the necessary documents, it’s time to submit the formal application. The bridge loan application process can take anywhere from 1 to 5 days, depending on the complexity of the deal and the lender’s requirements. This stage is critical as it initiates the formal evaluation of your loan request.

Submitting the Application: The borrower will submit a detailed application that includes property information, financials, and the proposed exit strategy.

Initial Review by Lender: The lender conducts a preliminary review of the property, the borrower’s financial standing, and the planned exit strategy. They will evaluate factors such as the value of the collateral, creditworthiness, and the loan-to-value (LTV) ratio.

Preliminary Underwriting: During this stage, the lender will begin conducting a basic underwriting process, which may involve a more informal assessment of the property’s value and the borrower’s ability to repay the loan.

During this stage, you will need:

Completed loan application

Financial statements and other financial documentation

Detailed property and project information

Any other relevant documentation (e.g., signed contracts, appraisal reports)

In commercial real estate, the initial review ensures that the loan fits within the lender’s risk parameters and is the foundation for further evaluations.

Stage 3: Lender Review and Due Diligence

After the initial review, the next step in the bridge loan approval process is the detailed property appraisal and full underwriting. The average processing time is three days, depending on the property’s complexity and value.

Property Appraisal: The lender typically commissions a full property appraisal to verify its market value. This process can be more detailed in commercial real estate, as the lender needs a comprehensive understanding of the property’s condition, location, and market dynamics.

Full Underwriting: The underwriting process will involve a deeper examination of the borrower’s financials, including credit history, past real estate investments, and the projected returns of the current project. The lender will also assess the risks involved in the transaction.

Review of Exit Strategy: Lenders will want to see a clear and viable exit strategy, whether it’s refinancing, selling the property, or another method. In commercial real estate, the proposed exit strategy can often be the deciding factor for approval.

Businesses must provide the following details during this stage:

Detailed property appraisal and inspection reports

Updated financial documents for both the borrower and any related entities (e.g., LLCs)

A clear timeline and process for the exit strategy

Proof of any income from the property (rent rolls, etc.)

At this stage, the lender ensures that the deal aligns with their risk profile and the potential for return on investment. In commercial real estate, this is an essential phase for guaranteeing the loan will be secure and repaid as per the agreed terms. The approval timeline for commercial bridge loans will ultimately depend on how well you have presented every detail.

Stage 4: Approval and Loan Offer

Once the appraisal and underwriting have been completed, the bridge loan enters the final approval and closing stages. This phase lasts 7 to 10 days, but it could be quicker or slower, depending on the lender and the complexity of the transaction.

Loan Approval: After reviewing all the necessary documentation, appraisals, and underwriting reports, the lender will provide the final loan approval. At this stage, they will confirm the loan terms, including the interest rate, repayment schedule, and special conditions.

Loan Agreement Signing: Both parties will sign the loan agreement, formalizing the terms and conditions. This includes defining the repayment structure, interest rates, and any early repayment or default penalties.

Disbursement of Funds: After the agreement is signed, the funds are disbursed to the borrower. In some cases, the funds may be expended in stages based on project milestones (e.g., when specific renovations are completed for a bridge loan used for construction).

This stage is the culmination of the approval process. In commercial real estate, investors can move forward with their plans once the loan is approved and the bridge loan disbursement process starts.

Stage 5: Loan Closing and Funding

The final stage of the bridge loan process is post-closing, which involves managing the loan until repayment. The timing and specifics of this stage depend on the exit strategy, which could vary based on whether the loan is paid off through refinancing, property sale, or other methods.

Loan Management: The borrower manages the loan throughout its term, ensuring that the property remains in good condition, any agreed-upon improvements are made, and the exit strategy is executed within the agreed-upon timeframe.

Repayment: Once the loan term is complete, it must be repaid in full. This could be done by selling the property, refinancing it into a more permanent loan, or by other means.

What are the Major Factors Impacting the Timeline of Bridge Loan Approval?

While bridge loans are suitable for quick funding, several factors can influence the approval timeline. Understanding these variables is crucial for commercial real estate investors to anticipate potential delays and keep their projects on track.

Lender Type

The type of lender you choose plays a vital role in determining the timeline for approval. Conventional lenders like banks and credit unions typically have stricter underwriting processes and require detailed financial reviews. This can make the approval process slower compared to private lenders. Private lenders, on the other hand, are more flexible and faster, often focusing on the property’s value and the borrower’s exit strategy.

Document Readiness

How prepared you are with required documentation can significantly impact the approval process. Essential documents often include detailed property information, financial statements, and a clear exit strategy. Submitting incomplete paperwork can lead to delays, as lenders may need additional time to request and review missing information.

Property Appraisal Delays

Property appraisal is a crucial step in bridge loan approvals, and delays often arise from scheduling challenges or discrepancies in appraisal values. Due to their complexity, commercial property appraisals can be time-intensive. They involve assessing property income and market trends.

Borrower Profile

Even though bridge loans are more lenient than conventional loans, the borrower’s creditworthiness and financial stability still matter. A strong borrower profile can give lenders confidence and expedite the approval process. Conversely, concerns about repayment ability may require additional reviews and discussions, which can slow things down.

Market Conditions

The volume of applications and the lender’s workload can also affect the timeline. During periods of high demand, such as a booming real estate market, lenders may face backlogs that delay approvals. Conversely, during slower periods, the process may move more quickly.

How to Expedite the Bridge Loan Approval Process?

Securing a bridge loan quickly is essential for commercial real estate investors operating on tight timelines. There are several strategies to consider to speed up the process.

First, organize and complete all necessary documents before submission. Lenders require detailed information, including financial statements, property details, and a well-defined exit strategy. Submitting incomplete paperwork leads to delays, so ensure everything is ready for review.

Next, consider working with lenders who specialize in bridge loans. These lenders are familiar with the urgency of such financing and often have dedicated systems to expedite approvals. Their expertise can make the difference between meeting or missing critical deadlines.

Finally, clear communication with the lender must be maintained throughout the process. Respond promptly to requests for additional information or clarifications to keep the process moving smoothly.

By following these steps, investors can minimize bottlenecks, gain access to funds more quickly, and stay on track to achieve their commercial real estate objectives.

Bridge Loan Approval vs. Traditional Loan Approval

The differences in timelines, requirements, and flexibility between bridge loan approval and traditional loan approval are striking, particularly for commercial real estate investors.

Timeline: Bridge loan approval can take as little as 72 hours, while conventional loans often take 30-60 days due to more intensive underwriting processes.

Requirements: Conventional loans typically have stricter qualification criteria, requiring high credit scores, extensive income verification, and detailed financial documentation. In contrast, bridge loans are more lenient. Although lenders still focus on credit quality and financial information, they also look at the property’s value and the borrower’s exit strategy.

Flexibility: Bridge loans offer greater flexibility in structuring terms to meet specific needs, such as interest-only payments or short-term durations. Conventional loans, while providing lower interest rates, lock borrowers into rigid long-term commitments, which may not align with the dynamic nature of real estate investments.

Fast-Track Your Financing with Bluestone Commercial Loans

Bluestone Commercial Loans is your trusted partner when time-sensitive commercial real estate opportunities arise. We specialize in providing fast, flexible, and reliable bridge loans tailored to meet the unique needs of real estate investors and business owners.

Why Choose Bluestone?

Quick Approvals: Get funding in as little as 72 hours.

Tailored Solutions: Flexible terms carefully curated for your specific project.

Expert Guidance: Utilize our industry expertise to navigate complex transactions.

Transparent Process: No hidden fees, just straightforward financing.

Whether acquiring new properties, covering renovation costs, or bridging cash flow gaps, our personalized approach ensures you won’t miss out on critical opportunities.

Don’t wait—let Bluestone help you move forward. Apply now to secure a bridge loan and keep your commercial real estate goals on track!

To provide the best experiences, we use technologies like cookies to store and/or access device information. Consenting to these technologies will allow us to process data such as browsing behavior or unique IDs on this site. Not consenting or withdrawing consent, may adversely affect certain features and functions.

Functional

Always active

The technical storage or access is strictly necessary for the legitimate purpose of enabling the use of a specific service explicitly requested by the subscriber or user, or for the sole purpose of carrying out the transmission of a communication over an electronic communications network.

Preferences

The technical storage or access is necessary for the legitimate purpose of storing preferences that are not requested by the subscriber or user.

Statistics

The technical storage or access that is used exclusively for statistical purposes.The technical storage or access that is used exclusively for anonymous statistical purposes. Without a subpoena, voluntary compliance on the part of your Internet Service Provider, or additional records from a third party, information stored or retrieved for this purpose alone cannot usually be used to identify you.

Marketing

The technical storage or access is required to create user profiles to send advertising, or to track the user on a website or across several websites for similar marketing purposes.